If you are considering buying property interstate, you are not alone. One in five Australian property investors are now looking beyond their own state to find better value, stronger rental returns and long term growth opportunities. With property prices continuing to...

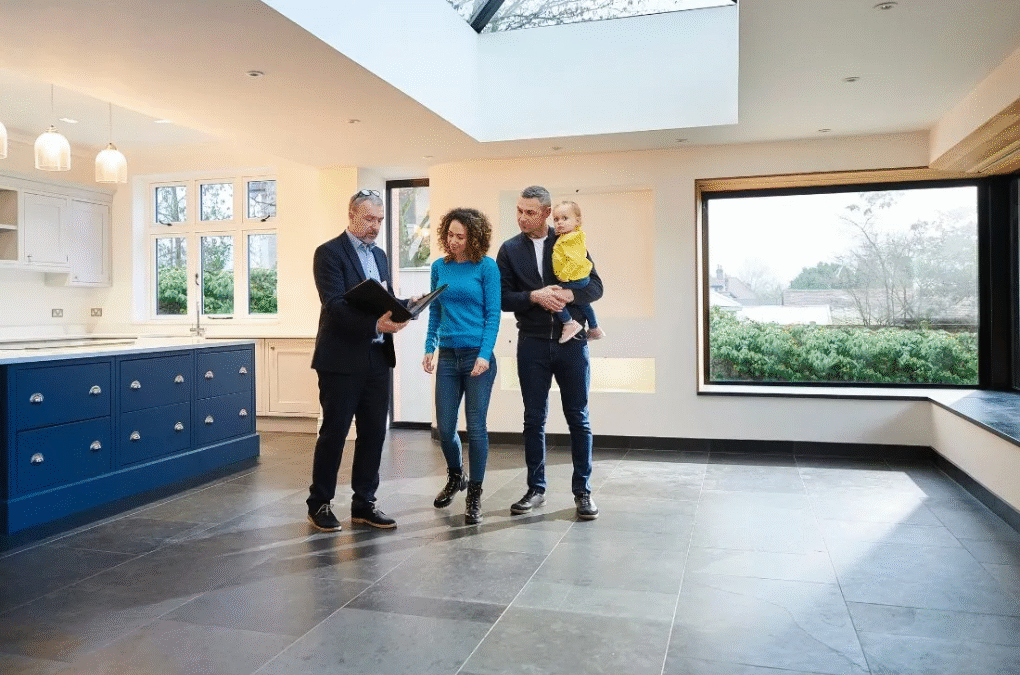

Finding the perfect property can be exciting, but not every home is easy to finance. Lenders view some dwellings as higher risk than others, which can affect how much you can borrow or whether a loan is approved at all. Understanding why certain properties attract...

Home lending in Australia has tightened considerably in the past few years. As property prices have climbed and household debt has risen, lenders have become far more thorough when assessing home loan applications. Many borrowers are surprised by the number of...

The increase in property listings Australia is creating a wave of opportunity for home buyers who have been struggling with limited choice over the past year. After a prolonged period of tight supply, new properties are finally hitting the market in higher volumes...

Are you considering a tree change and dreaming of more space, fresh air, and a slower pace of life? More Australians are exploring tree change homes in regional areas as a way to escape soaring city property prices. With median home values in our capital cities...